What does IRC stand for in tax law?

t. e. The Internal Revenue Code ( IRC ), formally the Internal Revenue Code of 1986, is the domestic portion of federal statutory tax law in the United States, published in various volumes of the United States Statutes at Large, and separately as Title 26 of the United States Code (USC). It is organized topically, into subtitles and sections ...

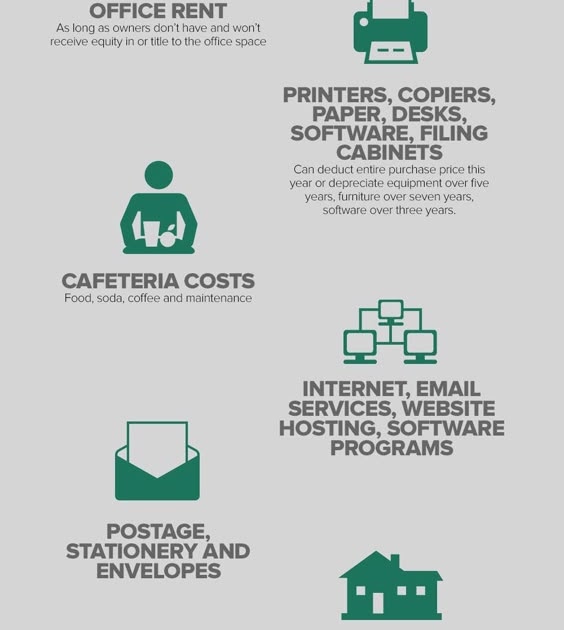

What is the tax treatment of R&D costs?

The research credit is an incremental credit that equals 20 percent of a taxpayer’s excess QREs (if any) for the taxable year over their base amount. The current carry-back is one year and carry-forward is 20 years (section 39).

How much will the R&D tax credit reduce tax revenue?

Jan 09, 2004 · 7. Employment Tax Treatment of Fringe Benefits Section F – Conclusion Discussion A. Definitions 1. Applicable Tax Exempt Organization. Regs. 53.4958-2T. I.R.C. 4958 imposes excise taxes on excess benefit transactions between disqualified persons and tax-exempt organizations described in either I.R.C. 501(c)(3) or I.R.C. 501(c)(4).

How do you determine the tax treatment of facilitative costs?

May 31, 2019 · Dear traceyrhering: Internal Revenue Code (IRC) Section 1341 repayment credit is one of the two options that a taxpayer has (the other being a tax deduction) when the taxpayer is faced with a situation known as a Claim of Right. A Claim of Right is, in simple layman's terms, basically the case where a taxpayer reported income as being taxable in one year, but then has …

What does IRC stand for Internal Revenue Code?

What is the tax treatment?

What is AMT taxable income?

Do I have to pay net investment income tax?

What are STT charges?

| Sr. No. | Taxable securities transaction | Tax Rate w.e.f. June 1, 2016 |

|---|---|---|

| 4a | Sale of an option in securities | 0.05 per cent |

| 4b | Sale of an option in securities, where option is exercised | 0.125 per cent |

| 4c | Sale of a futures in securities | 0.010 per cent |

Can STT be claimed as expenses in capital gain?

Is AMT in addition to regular tax?

Is AMT based on AGI or taxable income?

Who pays AMT tax?

What is the 3.8 tax on investment income?

Who pays the 3.8 investment tax?

What capital gains are excluded from net investment income tax?

What is the IRC code?

The Internal Revenue Code ( IRC ), formally the Internal Revenue Code of 1986, is the domestic portion of federal statutory tax law in the United States, published in various volumes of the United States Statutes at Large, and separately as Title 26 of the United States Code (USC).

What is the Internal Revenue Code?

The Internal Revenue Code ( IRC ), formally the Internal Revenue Code of 1986, is the domestic portion of federal statutory tax law in the United States, published in various volumes of the United States Statutes at Large , and separately as Title 26 of the United States Code (USC). It is organized topically, into subtitles and sections, covering income tax in the United States, payroll taxes, estate taxes, gift taxes, and excise taxes; as well as procedure and administration. Its implementing federal agency is the Internal Revenue Service .

What is the 1939 tax code?

The 1939 Code was published as volume 53, Part I, of the United States Statutes at Large and as title 26 of the United States Code. Subsequent permanent tax laws enacted by the United States Congress updated and amended the 1939 Code.

What is a research expenditure under section 41?

Section 41 requires that a taxpayer incur credit-eligible research expenditures "in carrying on" any "trade or business“. Thus, two conditions must be satisfied to qualify for the credit. First, as under section 174, there must be a qualifying trade or business. Second, the expense must be incurred in carrying on that trade or business.

What is research credit?

The research credit is an incremental credit that equals 20 percent of a taxpayer’s excess QREs (if any) for the taxable year over their base amount. The current carry-back is one year and carry-forward is 20 years (section 39). In many instances, verifying the base amount computation can have a more significant impact on audit results than the determination of allowable credit year QREs. Therefore, a review of the mechanical computation of the research credit is an essential step in the examination process, and should be performed in all examinations. All necessary documents, as determined during the pre-audit analysis, should be requested to insure that the taxpayer properly computed its research credit for all year (s) under examination.

What is gross receipts?

Section 41 (c) (6) does not provide a definition of the term “gross receipts”, other than to provide that gross receipts for any taxable year are reduced by returns and allowances made during the taxable year. In the case of a foreign corporation, only gross receipts effectively connected with the conduct of a trade or business within the United States, the Commonwealth of Puerto Rico (for amounts incurred after June 30, 1999), or any possession of the United States (same) are taken into account. As a result, a taxpayer may have included in gross receipts only the figure on Form 1120, line 1c. Treasury Regulation section 1.41-3 (c) (1) provides that for purposes of section 41, gross receipts means the total amount, as determined under the taxpayer's method of accounting, derived by the taxpayer from all its activities and from all sources (e.g., revenues derived from the sale of inventory before reduction for cost of goods sold) with the exception of the following items that are specifically excluded by Treasury Regulation section 1.41-3 (c) (2):

What is Section 41 F-3?

Section 41 (f) (3) generally requires an adjustment to be made to the base amount in the case of the acquisition or disposition of a major portion of a trade or business. Therefore, the examiner must ascertain whether the taxpayer made any acquisitions or dispositions that could affect the research credit computation. Compare the prior years and question any large discrepancies.

What is a 162 credit?

Under section 162, it is well established that the determination of the existence of a trade or business with respect to a partnership must be made at the partnership level, without regard to the existing businesses of the corporate or individual partners. The research credit regulations generally follow the section 162 approach to the application of the trade or business requirement to a partnership. Thus, if a newly formed research partnership initially has no active trade or business, the "in carrying on" requirement generally bars eligibility for the research credit.

What is a start up company?

A “start-up company” is generally defined as a company that did not have both gross receipts and QREs in at least three of the base period years, or the first taxable year in which there were both QREs and gross receipts began after December 31, 1983 . (The second provision did not take effect until July 1, 1996). For a start-up company, I.R.C. § 41 (c) (3) (B) assigns a fixed-base percentage of 3 percent. The 3 percent start-up rate continues each of the first five years beginning after 1993. In years 6 through 9, a statutory fraction of the ratio between aggregate QREs and aggregate gross receipts is used to determine the start-up’s fixed-base percentage. Only years in which the taxpayer has QREs are counted in this computation. See I.R.C. § 41 (c) (3) (B) (ii) to determine the start-up’s fixed base percentage after its initial 5-year period.

What is a 988 transaction?

The term “section 988 transaction” means any transaction described in subparagraph (B) if the amount which the taxpayer is entitled to receive (or is required to pay) by reason of such transaction —. I.R.C. § 988 (c) (1) (A) (i) —. is denominated in terms of a nonfunctional currency, or. I.R.C. § 988 (c) (1) (A) (ii) —.

What is foreign currency loss?

The term “foreign currency loss” means any loss from a section 988 transaction to the extent such loss does not exceed the loss realized by reason of changes in exchange rates on or after the booking date and before the payment date. I.R.C. § 988 (b) (3) Special Rule For Certain Contracts, Etc. —.

What is a cookie?

A cookie is a piece of data stored by your browser or device that helps websites like this one recognize return visitors. We use cookies to give you the best experience. Some cookies are also necessary for the technical operation of our website. If you continue browsing, you agree to this site’s use of cookies.

How much will the R&D tax credit reduce taxes?

According to the Joint Committee on Taxation’s (JCT) most recent tax expenditure report, the R&D tax credit will reduce tax revenue by about $11.8 billion in 2020— $10.6 billion for corporations and $1.2 billion for individuals. [4] The R&D tax credit was first established in 1981, in the Economic Recovery Tax Act (ERTA).

Does the R&D tax credit increase spending?

The economic literature on the R&D tax credit suggests that it increases R&D spending, although the magnitude of that increase and how much of that new research translates to new innovation is more ambiguous.

Why is R&D important?

Investment in research and development (R&D) is central for driving long-term technological change and innovation. The R&D tax credit and immediate expensing for R&D spending are two important ways the federal tax code provides incentives for R&D investment.

What is the main driver of long-term economic growth and increases in living standards?

Technological innovation is the main driver of long-term economic growth and increases in living standards. [1] It is difficult to have ongoing technological innovation without investing in research and development (R&D).

When was the R&D tax credit established?

The R&D tax credit was first established in 1981, in the Economic Recovery Tax Act (ERTA). The initial credit equaled 25 percent of a corporation’s research spending in excess of its average research spending in the preceding three years, or alternatively, 50 percent of its current-year spending. [5] .

Can you deduct R&D expenses?

Under current law, firms can choose to fully deduct R&D costs from their taxable income in the year in which they are incurred.

What is tax credit?

A tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly. Taxable income is the amount of income subject to tax, after deductions and exemptions.