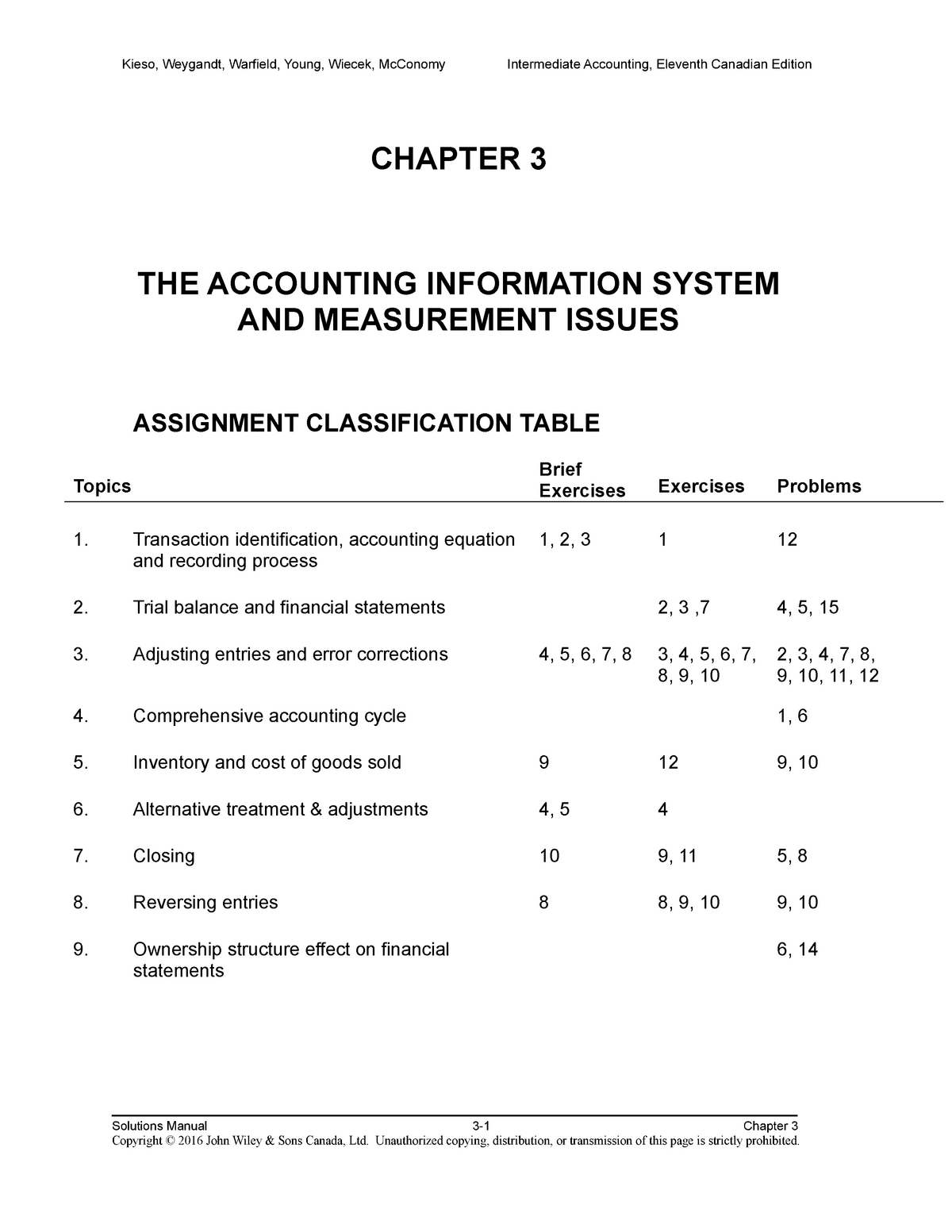

What is the impact of alternative accounting treatments on financial statements?

Using the accounting alternative would typically result in significant differences in the financial statements compared to financial statements that do not include the alternative. As a result, policy note disclosures need to be clear as to the accounting approach used when alternative accounting treatments are available.

How does the accounting alternative provide relief to private companies?

This may provide relief to private companies by eliminating the requirement to evaluate goodwill impairment triggering events as they occur during the reporting period. The guidance under the accounting alternative affects the timing of an entity’s evaluation of the occurrence of goodwill impairment triggering events.

What is the accounting alternative for impairment of goodwill?

The accounting alternative allows private companies/NFPs to evaluate goodwill impairment triggering events only as of the end of the reporting period, whether interim or annual, and to recognize and measure any resulting goodwill impairment as of that date, if necessary.

What is the accounting treatment for equity securities?

The accounting treatment was introduced to improve accounting for certain financial assets and provides an accounting framework for valuing an equity security investment in the absence of a readily determinable fair value.

What are alternative accounting treatments?

These include accrual, cash, special and hybrid. The two most common methods are accrual and cash. The special and hybrid methods are used for alternative accounting in special circumstances.

What is an alternative to GAAP accounting?

An Alternative to GAAP One such alternative is the Financial Reporting Framework for Small- and Medium-Sized Entities (FRF for SMEsTM), which is a comprehensive financial reporting framework promulgated by the American Institute of CPAs (AICPA).

What is accounting treatment in accounting?

What is Accounting Treatment: An asset that is completely depreciated and continues to be used in the business concern will be reported on the balance sheet (B/S) at its cost along with its accrued depreciation. There will be no depreciation expense maintained after the asset is completely depreciated.

What are the 3 basic tools for financial statement analysis?

Three common analysis tools are used for decision-making; horizontal analysis, vertical analysis, and financial ratios.

What is goodwill accounting alternative?

The accounting alternative allows private companies/NFPs to evaluate goodwill impairment triggering events only as of the end of the reporting period, whether interim or annual, and to recognize and measure any resulting goodwill impairment as of that date, if necessary.

Can we amortize goodwill?

Goodwill can be amortized over 10 years or less, in which case the impairment test is simplified in addition to being trigger-based. In 2016 the FASB launched a project to simplify goodwill impairment testing for all companies, while maintaining its usefulness. This is a two-phase project.

What are the 4 types of accounting?

Discovering the 4 Types of AccountingCorporate Accounting. ... Public Accounting. ... Government Accounting. ... Forensic Accounting. ... Learn More at Ohio University.

What are the three accounting methods?

And, there are three accounting methods: accrual basis, cash basis, and modified cash basis. Before we can talk about which types of businesses use specific accounting methods, let's briefly go over the basics.

What are the 4 types of expenses?

Terms in this set (4)Variable expenses. Expenses that vary from month to month (electriticy, gas, groceries, clothing).Fixed expenses. Expenses that remain the same from month to month(rent, cable bill, car payment)Intermittent expenses. ... Discretionary (non-essential) expenses.

What are the 5 types of financial statements?

The 5 types of financial statements you need to knowIncome statement. Arguably the most important. ... Cash flow statement. ... Balance sheet. ... Note to Financial Statements. ... Statement of change in equity.

What are the 5 methods of financial statement analysis?

Five Financial Statement Analysis TechniquesTrend analysis:Common-size financial analysis:Financial ratio analysis:Cost volume profit analysis:Benchmarking (industry) analysis:

What are the three main types of financial statements?

The balance sheet, income statement, and cash flow statement each offer unique details with information that is all interconnected. Together the three statements give a comprehensive portrayal of the company's operating activities.

What is GAAP accounting?

The Financial Accounting Standards Board (FASB) has issued two updates to generally accepted accounting principles (GAAP) intended to reduce the cost and complexity of financial statement preparation for private companies that elect either or both of the alternatives. As outlined in Accounting Standards Update (ASU) 2014-02, Intangibles—Goodwill and Other (Topic 350): Accounting for Goodwill, and ASU 2014-03, Derivatives and Hedging (Topic 815): Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach, the alternative standards streamline the method for goodwill impairment and make it easier for certain interest rate swaps to qualify for hedge accounting.

Why use simplified hedge accounting?

Because settlement value may be easier to determine, private companies that apply simplified hedge accounting may enjoy cost savings from this measurement alternative. The accounting alternative can be applied to both existing and new qualifying interest rate swaps and it can be applied on a swap-by-swap basis.

What is the FASB PCC?

The Financial Accounting Foundation (the FASB’s parent organization) formed the PCC in May 2012 to improve the process of setting accounting standards for private companies that prepare their financial statements in accordance with GAAP. In December 2013 the FASB and the PCC released the Private Company Decision-Making Framework: A Guide ...

When does goodwill amortize?

A company will amortize existing goodwill starting at the beginning of the period of adoption (when the alternative is elected), and new goodwill recorded after the beginning of the annual period of adoption will begin amortization upon its recognition.

Do private companies have to use GAAP?

Even if a private company is otherwise eligible for the alternatives, financial statement users (including regulators, lenders, and other credito rs) may require the company to continue applying traditional GAAP accounting standards as though it were a public business entity.

Can a private company get a fixed rate loan?

A private company can find it difficult to obtain a fixed-rate loan . To avoid the risk of rising interest rates, a company must often enter into an interest rate swap (a derivative instrument) to economically convert a variable-rate loan into a fixed-rate loan.

Does GAAP require a hedge?

Existing GAAP requires the company to recognize all derivative instruments in its balance sheet as either assets or liabilities measured at fair value. If certain requirements are met, a company may elect cash flow hedge accounting to mitigate income statement volatility for changes in the fair value of the swap.

When new accounting guidance has been issued but is not yet effective as of the balance sheet date, what is the answer

When new accounting guidance has been issued but is not yet effective as of the balance sheet date, companies often disclose the issuance of the new accounting guidance, as follows: Date the entity must adopt the new guidance or, if early adoption is permitted, the date that it plans to adopt it.

What is controlling financial interest?

Currently, U.S. GAAP requires an entity to consolidate another entity in which it has a controlling financial interest. There are two primary models for assessing whether there is a controlling financial interest—the voting interest model and the VIE model. Under the voting interest model, the principle for a controlling financial interest is contractual or other legal arrangements that provide ownership of a majority voting interest. Under the VIE model, an entity is deemed to have a controlling financial interest when it has both the power to direct the activities of the entity and the obligation to absorb losses or the right to receive benefits of the entity.

When did the FASB change the consolidation topic?

In October 2018, the FASB amended the Consolidation topic of the Accounting Standards Codification. Under the amended guidance, a nonpublic entity has the option to exempt itself from applying the variable interest entity consolidation model to qualifying common control arrangements.

Can an entity change its accounting principles?

Generally, reporting entities are allowed to change accounting principles only if the change is required through amendments to the ASC or when reporting entities can justify the use of an allowable alternative accounting principle on the basis that it is preferable.

What is hedge accounting?

Hedge accounting is generally considered the preferred accounting treatment, as gains or losses on the item being hedged (in this case, the original variable - rate debt) are offset by losses or gains on the hedging instrument (the receive - variable / pay - fixed interest rate swap).

Why do private companies shy away from hedge accounting?

This reduces income statement volatility. Because the rules for hedge accounting can be difficult for companies with limited resources to apply, private companies might shy away from using hedging strategies to reduce risk, even when they do in fact qualify.

How long does goodwill amortize?

Under private company treatment, rather than carrying goodwill on the books at its original value and testing it for impairment annually, private companies may elect to amortize goodwill on a straight - line basis over 10 years (or less, if the company demonstrates that another useful life is more appropriate).

Is it too late to take advantage of the opportunities they provide to simplify private company accounting?

The good news is that even though the four private company GAAP alternatives that have been created were issued in 2014, it's not too late to take advantage of the opportunities they provide to simplify private company accounting. In 2016, following the PCC's initiative, FASB eliminated the effective dates for the four private company GAAP ...

Do private companies ignore goodwill?

Users of private company financial statements told the PCC that they generally ignore goodwill and its impairment when analyzing financial strength and operating performance. This led to a more simplified approach to impairment.

Does PCC advise FASB?

In addition to researching and making recommendations on private company alternatives for existing GAAP requirements, the PCC also advises FASB as new standards are promulgated. In some cases, FASB has chosen the "alternative" approach for all entities.

What is a nonrefundable advance?

Defer the recognition of any nonrefundable advance payments that will be used for research and development activities, and recognize them as expenses when the related goods are delivered or services performed.

What is core accounting?

The core accounting rule in this area is that expenditures be charged to expense as incurred. Examples of activities typically considered to fall within the research and development functional area include the following: Research to discover new knowledge. Applying new research findings.

What’s Happening?

Private Company Accounting Alternative

- Currently, U.S. GAAP requires an entity to consolidate another entity in which it has a controlling financial interest. There are two primary models for assessing whether there is a controlling financial interest—the voting interest model and the VIE model. Under the voting interest model, the principle for a controlling financial interest is contr...

Disclosure Requirements

- A private company (reporting entity) that elects the accounting alternative must provide the following disclosures: 1. The nature and risks associated with a reporting entity’s involvement with the legal entity under common control. 2. How a reporting entity’s involvement with the legal entity under common control affects the reporting entity’s financial position, financial performan…

Other Disclosure Considerations

- Disclosure of New Guidance before Effective Date When new accounting guidance has been issued but is not yet effective as of the balance sheet date, companies often disclose the issuance of the new accounting guidance, as follows: 1. Existence of the new accounting guidance 2. Date the entity must adopt the new guidance or, if early adoption is permitted, the d…

Effective Date and Transition

- The amendments in ASU 2018-17 are effective for a private company for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021. Entities are required to apply the amendments in ASU 2018-17 retrospectively with a cumulative-effect adjustment to retained earnings at the beginning of the earliest period present…

We Can Help

- Elliott Davis is ready to answer your questions and provide the resources and information you need. In the meantime, if you have questions, please contact your Elliott Davis advisor. The information provided in this communication is of a general nature and should not be considered professional advice. You should not act upon the information provided without obtaining specifi…