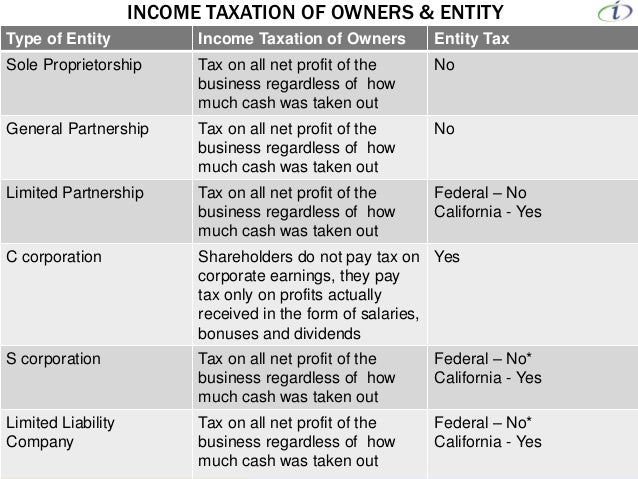

What happens when an S Corp terminates?

When an entity loses its S corporation status, the entity becomes treated for U.S. federal tax purposes as a C corporation. In general, the S corporation's tax year is deemed to end the day before the failure to adhere occurs and the C corporation's tax year begins on the day of the failure to adhere.

What happens to a corporation's tax attributes in a complete liquidation?

What happens to a corporation's tax attributes (e.g. earnings and profits, NOL carryforwards) in a complete liquidation? A corporation's tax attributes generally disappear in a complete liquidation, except when Sections 332 and 334 (b) (1) apply to the liquidation of a subsidiary. You just studied 18 terms!

What are the treatments for loans from shareholders when dissolving an S Corp?

Since S corporations typically pass corporate profits and losses through to shareholders, who then report on their personal tax returns, the shareholder will have to report the loan as ordinary income.

What are the tax consequences of dissolving a corporation?

The tax consequences of liquidating a C corporation holding appreciated assets can be adverse. With maximum federal corporate rates of 35%, maximum individual rates on long-term capital gains of 20%, and the net investment income tax rate of 3.8%, the combined federal tax burden can approach 60% of taxable income.

Are corporate liquidations taxable?

The primary difference between an S corporation or C corporation is that any gain recognized by the S corporationon liquidation increases the shareholders' basis in their stock, thus reducing the amount of gain on which it is taxable.Oct 1, 2020

How do you liquidate a corporation for tax purposes?

Typically, such a transaction is accomplished in three stages:The corporation makes a direct sale of its assets to the buyer (or buyers).The company pays off all its debts (including any tax bills).The corporation distributes the remaining sales proceeds to the shareholders in complete liquidation of the entity.Apr 3, 2018

How do you appreciate property out of an S-Corp?

There are two types of appreciated properties: real property (real estate) and intangible property (stocks, bonds, and the like). To remove property from a corporation, ownership/title must change. Removal is generally by sale or by distribution to shareholders.Sep 26, 2017

Can a shareholder loan be forgiven?

If a principal shareholder's cancellation of debt owed to the shareholder by the corporation was forgiven in order to improve the corporation's financial position, the debtor corporation is treated by Sec. 108(e)(6) as having satisfied the debt with cash equal to the shareholder's adjusted basis in the debt.Aug 31, 2008

How does repayment of shareholder loan affect basis?

Full or partial cash repayment of the debt by the corporation reduces the shareholder's loan basis. (Repayment with property other than cash is beyond the scope of this item.) If the debt basis has previously been reduced to zero, all the subsequent repayment is treated as taxable income to the shareholder.Sep 30, 2008

What happens to retained earnings when a corporation closes?

When businesses close, the retained earnings will be distributed as part of the asset sale to settle outstanding liabilities.Aug 19, 2020

Can you file a tax return for a dissolved company?

Upon the completion of your company being dissolved, you are required to file a final tax return with the IRS. If you have a C corporation, you will file form 1120. If you have an S corporation, you will file form 1120-S.

Can I use a bank account after dissolving an S corporation?

After dissolution, you cannot use the funds remaining in your business bank account for new business. LLC members no longer have the authority to conduct business or do anything that would indicate that the LLC is still active. Your bank account can cover only essential winding up affairs.

Who pays for leasehold improvements?

Repairs and upgrades that fall under leasehold improvements can be paid for by either the landlord or the tenant, usually as outlined in the lease. If the landlord pays for the improvements, he can depreciate the cost of those modifications as a business expense. Like other expenditures, leasehold improvements are considered the cost ...

How long can you depreciate a leasehold?

Under the new law, improvements made to the inside of the building that are nonstructural in nature can be depreciated over a 15-year period as long as they were made “after the building is originally placed in service.”

Is leasehold improvement depreciation?

If, on the other hand, the tenant makes the improvements and isn’t reimbursed for them, that tenant can enjoy the leasehold improvement depreciation that would have otherwise gone to the landlord.

What is shareholder basis?

The shareholder’s basis in assets received is their FMV at the time of the distribution. Basis is not affected by the shareholder’s assuming corporate liabilities or receiving corporate property that is subject to a liability (Sec. 334 (a); see also Ford ).

Can a general business credit be recaptured?

General business credits can be subject to recapture as the result of the liquidation of an S corporation. For example, the low-income housing credit (LIHC) authorized by Sec. 42 is a business tax credit for residential rental property that qualifies as low-income housing under detailed statutory criteria.

Does liquidation terminate S election?

The liquidation process itself does not terminate the company’s S election. Therefore, passthrough items in the year of liquidation are allocated under the normal per-share, per-day rule of Sec. 1377 (a) (1). However, a bunching of income can occur in the year of liquidation of a fiscal-tax-year S corporation if the final liquidating distribution occurs on a date other than the last day of the fiscal year. This can result in the shareholders reporting more than 12 months of passthrough income in a single year.

Is dividend a liquidation?

The dividend rules that otherwise apply to corporate distributions are not applicable to distributions in complete liquidation. Distributions received by the shareholder are treated as payment in full for the exchange of stock. The shareholder’s adjusted basis in the stock is subtracted from the cash and fair market value (FMV) ...

When is the S corp tax return due?

The final S corporation tax return (Form 1120S, U.S. Income Tax Return for an S Corporation) is due on March 15, 2020, but can be extended to Sept. 15. Assuming the corporation extends the due date of the return, the PTTP will begin on April 10, 2019, and end on Sept. 15, 2020 (even if the return is filed prior to Sept. 15). Example 2. ...

When does PTTP apply?

The PTTP applies when the S election terminates, regardless of whether the termination occurs voluntarily because the corporation revokes its S election or involuntarily (e.g., an ineligible shareholder acquires stock in the corporation). Measurement of the PTTP is illustrated in the following examples. Example 1.

What is the 120 day period?

One year after the last day, or. The due date, including extensions, of that last year's tax return; The 120-day period beginning on the date of a determination that the corporation's S election had terminated ...

Is a retail lease considered gross income?

Specifically, Section 110 provides that cash or an amount treated as a rent reduction, received by a retail tenant is not gross income if the amount is used for qualifying construction of leasehold improvements.

Can a landlord depreciate the cost of improvements?

One option would be for the landlord to pay for the improvements, in which case they would own the improvements and would depreciate the cost of the improvements over the statutorily prescribed life. There would be no tax consequences for the tenant in this scenario unless the tenant also contributes to the cost of improvements.

What is leasehold improvement?

Leasehold improvements are defined as the enhancements paid for by a tenant to leased space. Examples of leasehold improvements are: Leasehold improvements generally revert to the ownership of the landlord upon termination of the lease, unless the tenant can remove them without damaging the leased property. An example of leasehold improvements is ...

Is leasehold improvement amortized?

Technically, you are amortizing leasehold improvements rather than depreciating them. The reason is that the landlord owns the improvements, so you are only exercising an intangible right to use the improvements during the term of the lease - and intangible assets are amortized, not depreciated.

The Problem

Where an S corporation's assets are sold or the S corporation stock is sold and a Sec. 338 (h) (10) election is made, the basis in the assets must be allocated to the cash portion distributed in liquidation for immediate income recognition and to the note portion in determining future income recognition as cash is collected on the note.

The Solution

Where there is an asset or deemed asset sale followed by a liquidation that includes installment obligations, the adviser must be aware of the basis allocation rule discussed above. One solution is to structure the transaction so no cash is received at closing.

Conclusion

The above examples are oversimplifications of what would occur in practice. However, the purpose is to illustrate the trap, albeit seemingly unintended, that lies within Sec. 453 (h) as it relates to distributions of installment obligations of a liquidating S corporation.

When is a loss recognized at the corporate level?

No loss is recognized at the corporate level when an S corporation distributes property with an FMV that is less than its basis. (Conversely, a loss can be recognized if the distribution is in liquidation of the corporation.)

What is a related person?

For these purposes, the term “related person” includes an S corporation and a shareholder who owns (directly or indirectly) more than 50% of its stock, as well as an S corporation and another corporation (C or S corporation) if the same persons own more than 50% of the stock of each corporation (Sec. 1239 (b)).

Is depreciation of property considered ordinary income?

If property sold or exchanged between related parties is depreciable by the buyer, any gain recognized on the sale or exchange is treated as ordinary income (Sec. 1239). This rule applies even if (1) the property was not depreciable by the seller, (2) the buyer does not actually depreciate it, or (3) the parties have no tax avoidance motives.

Can an S corporation distribute cash?

An S corporation can distribute property (as well as cash) to its shareholders. If property is distributed, the amount of the distribution is considered to be the property’s fair market value (FMV) (Sec. 301 (b)). The tax attributes of the distribution are generally determined as if the distribution had been made in cash.