The taxes are different for "Unrecaptured Section 1250 Gain" than regular long-term capital gain. The Unrecaptured Section 1250 Gain is taxed at your regular tax bracket, up to a maximum of 25%. Long-term capital gains are taxed at lower rates, usually 15%.

Full Answer

Is 1250 recapture ordinary income?

The entire gain is from depreciation recapture. It is done on an installment sale, however, according to Form 6252 instructions: Any ordinary income recapture under section 1245 or 1250 (including sections 179 and 291) is fully taxable in the year of sale even if no payments were received.

Is there depreciation recapture on 1250 property?

Yes, since rental properties are depreciable they are subject to unrecaptured Section 1250 gains, so any depreciation must be recaptured when the property is sold. How do you calculate 1250 depreciation recapture? Unrecaptured section 1250 gains are limited to 25% for 2019.

What is the difference between 1245 and 1250 depreciation recapture?

For §1245 property and §1250 property held for less than one year, the depreciation limitation is the amount of depreciation or amortization actually taken For §1250 property held for more than one year, the depreciation limitation is the amount of depreciation taken over the amount allowable under the straight-line method

How to calculate Section 1250 recapture real estate?

Key Takeaways

- An unrecaptured section 1250 gain is an income tax provision designed to recapture the portion of a gain related to previously used depreciation allowances.

- It is only applicable to the sale of depreciable real estate.

- Unrecaptured section 1250 gains are usually taxed at a 25% maximum rate.

- Section 1250 gains can be offset by 1231 capital losses.

Is Unrecaptured section 1250 gain taxable?

The portion of any unrecaptured section 1250 gain from selling section 1250 real property is taxed at a maximum 25% rate.

Why does 1250 recapture no longer apply?

Because straight–line depreciation has been required for all depreciable realty purchased after 1986, there is no section 1250 recapture on that property, and the gain on its disposal is eligible for long–term capital gain treatment under section 1231.

Is unrecaptured 1250 gain ordinary income?

This Section 1250 depreciation recapture is taxed at ordinary income rates. Any gain in excess of the amount treated as ordinary income because of Section 1250 recapture, but not exceeding the total depreciation claimed, is "unrecaptured Section 1250 gain".

How is unrecaptured 1250 gain treated?

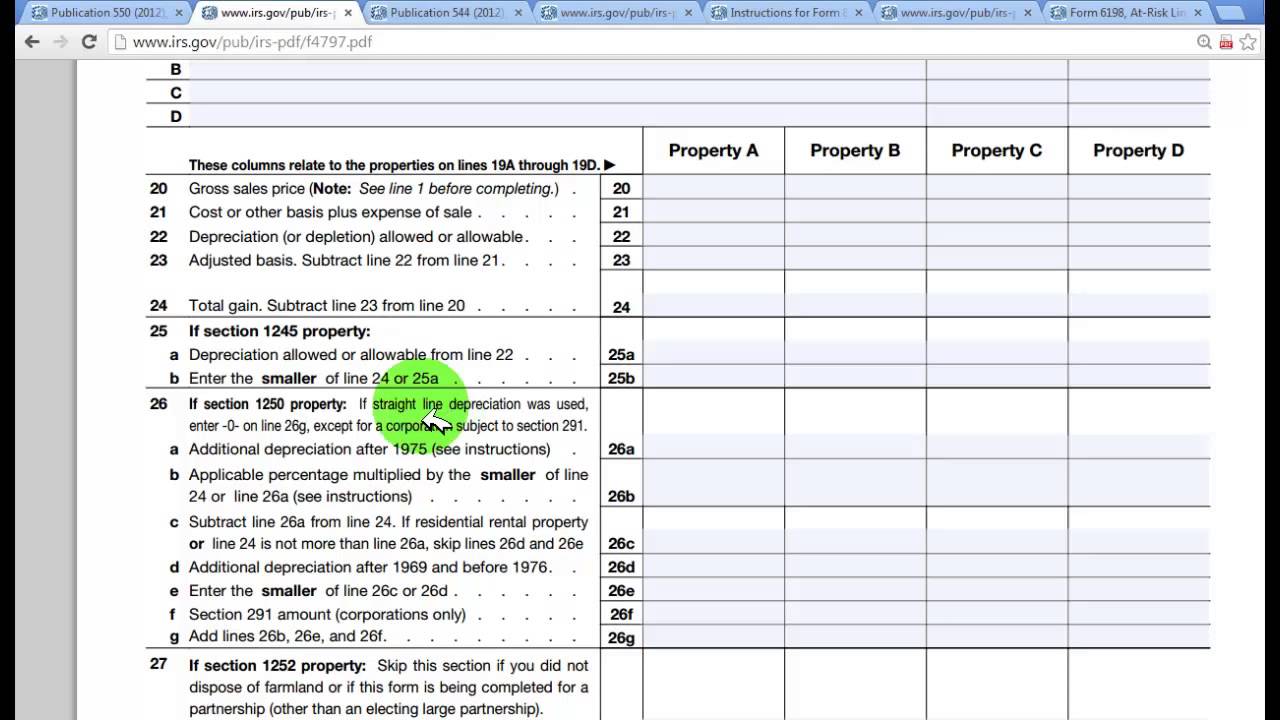

You report uncaptured Section 1250 gains on Form 4797, then transfer that total to Schedule D. 4 The instructions for Schedule D include detailed explanations and worksheets to help you make your calculations. Enter the resulting tax amount on line 16 of your Form 1040 tax return.

How is unrecaptured 1250 gain for individuals similar to depreciation recapture how is it different?

How is unrecaptured §1250 gain for individuals similar to depreciation recapture? How is it different? Unrecaptured §1250 gain is similar to depreciation recapture in that the lesser of accumulated depreciation or the gain realized on the sale is separated from the §1231 gain.

Is unrecaptured 1250 gain subject to net investment income tax?

The gain attributable to the depreciation may be subject to the 25% unrecaptured Section 1250 gain tax rate. Additionally, taxable gain on the sale may be subject to a 3.8% Net Investment Income Tax.

Where do I enter Unrecaptured Section 1250 gain?

Where do I enter Section 1250 Unrecaptured Gain? Use screen Unrecaptured Section 1250 Gain on the Assets-Sales-Recapture tab. It is available in both 1065 and 1120S packages. If there is a capital gain on the return, Wks 1250 may be generated.

Is section 1250 gain ordinary income?

Section 1250 of the U.S. Internal Revenue Code establishes that the IRS will tax a gain from the sale of depreciated real property as ordinary income, if the accumulated depreciation exceeds the depreciation calculated with the straight-line method.

Is depreciation recapture always taxed at 25?

Depreciation recapture is the portion of your gain attributable to the depreciation you took on your property during prior years of ownership, also known as accumulated depreciation. Depreciation recapture is generally taxed as ordinary income up to a maximum rate of 25%.

When 1250 property is disposed of how would you treat the gain?

If, in the case of a disposition of section 1250 property, the property is treated as consisting of more than one element by reason of paragraph (3), then the amount taken into account under subsection (a) in respect of such section 1250 property as ordinary income shall be the sum of the amounts determined under ...

How do you calculate 1250 depreciation recapture?

Unrecaptured section 1250 gains are limited to 25% for 2022. The total amount of tax that the taxpayer will owe on the sale of this rental property is (0.15 x $155,000) + (0.25 x $110,000) = $23,250 + $27,500 = $50,750. The depreciation recapture amount is, thus, $27,500.

Does Section 1250 recapture qualify for Qbi?

No. The depreciation recapture portion for the sale of a rental property is section 1250 gain and therefore not part of QBI.

Does 1250 recapture still apply?

Key Takeaways An unrecaptured section 1250 gain is an income tax provision designed to recapture the portion of a gain related to previously used depreciation allowances. It is only applicable to the sale of depreciable real estate. Unrecaptured section 1250 gains are usually taxed at a 25% maximum rate.

When 1250 property is disposed of how would you treat the gain?

If, in the case of a disposition of section 1250 property, the property is treated as consisting of more than one element by reason of paragraph (3), then the amount taken into account under subsection (a) in respect of such section 1250 property as ordinary income shall be the sum of the amounts determined under ...

What is the Section 1245 recapture rule?

Section 1245 is a mechanism to recapture at ordinary income tax rates allowable or allowed depreciation or amortization taken on section 1231 property. Allowable or allowed means that the amount of depreciation or amortization recaptured is the greater of that taken or that could have been taken but was not.

Is 15 year property subject to recapture?

This means that these four types of 19-year (or 18- or 15-year) ACRS real property and low-income housing that have specifically defined as subject to recapture under Section 1250, and that all other ACRS real property is subject to recapture under Section 1245.

What is the tax rate for Sec 1250?

But the amount of depreciation claimed on Sec 1250 property that is not recaptured as ordinary income under the Sec1250 recapture rules is unrecaptured section 1250 gain, and is subject to a special capital gain tax rate of 25%.

What is the LTCG tax rate?

The balance of the gain, if any, is taxed at the normal capital gains rate based upon the individual’s regular tax rate, as follows: The LTCG tax rate is zero to the extent the taxpayer’s taxable income bracket is below 25%. The LTCG tax rate is 15% to the extent the taxpayer’s taxable income bracket is above 25% and below 39.6%.

Is Sec 1250 recaptured?

However, this means that as long as the property is being depreciated using a straight-line method and held over a year, there is no Sec 1250 recapture but there will be “unrecaptured Sec 1250 gain,” which is taxed at a maximum rate of 25%. The balance of the gain, if any, is taxed at the normal capital gains rate based upon ...

What is Section 1250 gain?

Unrecaptured Section 1250 gain is the amount of the depreciation taken on the property -- limited to the actual gain on the sale -- that is not recaptured as ordinary income under Section 1250. To illustrate, our building has $50,000 of depreciation, and upon it's sale, the building generates $150,000 of gain.

How to determine if you have a Section 1231 gain or loss?

But in order to determine if you have net Section 1231 gain or loss, you first have to identify your "Section 1231 assets.". As you peruse your tax balance sheet, you're looking for two broad categories of assets: 1. All depreciable assets that have been held for longer than one year are considered Section 1231 assets.

What is a 1245 asset?

Section 1245 assets are the Section 1231 assets that are depreciable personal property. If you'll remember, amortizable Section 197 intangibles are also treated as Section 1231 assets because they are treated as depreciable assets; thus, these assets are also included in the definition of Section 1245 assets.

What is Section 1231?

Section 1231 is a categorization provision -- once identified, all gain and loss from "Section 1231 assets" are netted together with ideal results: a net gain is capital, while a net loss is ordinary . Sections 1245 and 1250 are "recharacterization" provisions -- assets that meet the definition of either of these two provisions may potentially have all or a portion of gain from their sale recharacterized as either ordinary income or gain that is taxed at 25%. Segregating between the two provisions is not particularly difficult: Section 1245 assets are depreciable personal property or amortizable Section 197 intangibles; Section 1250 assets are real property, whether depreciable or not.

Is a Section 1231 loss ordinary?

Section 1231 is a very taxpayer-friendly provision, because the character of a Section 1231 gain or loss is a chameleon. If the sum of a taxpayer's gains and losses from the sale of Section 1231 assets is a net gain, the gain is capital, and provided the selling entity isn't a C corporation, is taxed at favorable rates. On the flip side, if the sum of a taxpayer's gains and losses from the sale of Section 1231 assets is a net loss, the loss is ordinary. That's right -- Section 1231 gains are capital; Section 1231 losses ordinary. This is the Holy Grail of tax planning -- capital gain/ordinary loss.

Is Section 1231 a chameleon?

Section 1231 is a very taxpayer-friendly provision, because the character of a Section 1231 gain or loss is a chameleon. If the sum of a taxpayer's gains and losses from the sale of Section 1231 assets is a net gain, the gain is capital, and provided the selling entity isn't a C corporation, is taxed at favorable rates.

Is the $5,000 depreciation ordinary income?

The net amount of $5,000 is recharacterized as ordinary income under Section 1245, or "recaptured," because the $5,000 of depreciation that created the gain -- by driving the basis below the FMV -- was ordinary in nature, and so now that gain must be ordinary as well.