There are five types of accounting treatment of goodwill at the time of admission of a new partner:

- When the amount of goodwill is brought in cash and not recorded in books.

- When the new partner brings his share of goodwill in cash and is retained in business.

- When the new partner does not bring his share of goodwill in cash.

- When goodwill already exists in the books.

- When goodwill is raised at its full value.

Full Answer

What is the accounting treatment for goodwill?

Goodwill accounting treatment. In accounting, we treat goodwill as an intangible asset just as it has been highlighted above. It does not include identifiable assets that are capable of being separated from the acquired company and sold, transferred, exchanged, licensed, or rented. In essence, goodwill is a representation of assets that are not ...

How to write off Goodwill?

What Happens To Goodwill On A Balance Sheet? On an acquiring company’s balance sheet, goodwill can be classified as an intangible asset, corresponding to long-term assets. As Goodwill cannot be classified as a tangible asset like real estate or equipment ...

How to account for goodwill?

Accounting for business goodwill. Accounting for business goodwill in your books requires that you subtract the fair market value of tangible assets from the total worth of the business. Goodwill is, therefore, equal to the cost of acquisition minus the value of net assets.

Is goodwill a depreciable asset?

The reason which is given by the authority for such amendment was that “It is seen that goodwill, in general, is not a depreciable asset and in fact depending upon how the business runs; goodwill may see appreciation or in the alternative no depreciation to its value.

What is treatment of goodwill in accounting?

The goodwill can be calculated as the difference between the business value or the purchasing cost and the value of the assets of the company which appear in the corresponding accounts.

What is goodwill and its treatment?

Goodwill, in accounting terms, is referred to as an intangible asset that represents the value created by the firm.

What is the treatment of goodwill in dissolution?

There is no need to give a special treatment to goodwill in case of dissolution. It should be treated like any other asset. If it already appears in books, it will be transferred, like all other assets, to the debit side of Realisation Account. If it does not so appear, there is no question of transfer.

How do you treat goodwill in financial statements?

If the value of goodwill remains the same or increases, the amount entered remains unchanged. The amount can change, however, if the goodwill declines. If that's the case, the company undergoes what's known as goodwill impairment.

What goodwill means?

Goodwill is an intangible asset that is associated with the purchase of one company by another. Specifically, goodwill is the portion of the purchase price that is higher than the sum of the net fair value of all of the assets purchased in the acquisition and the liabilities assumed in the process.

What are the accounting treatment of goodwill class 12?

1. Accounting Treatment of Goodwill When a new partner is admitted, his share in future profits of the firm is equal to the sacrifice of profit by an existing partner or partners of the firm, the amount he pays to compensate this sacrifice is called goodwill.

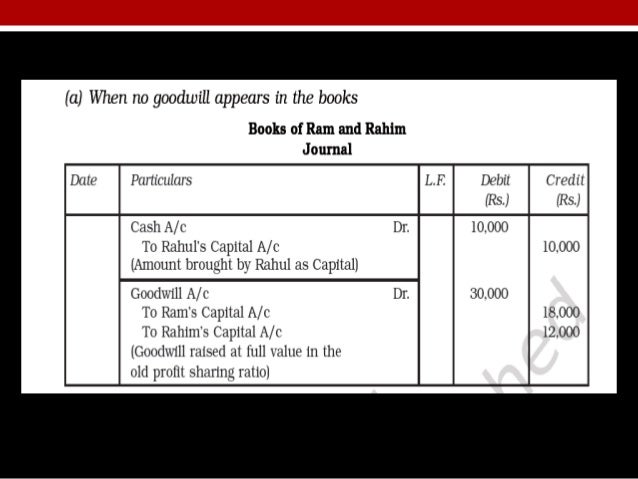

When goodwill is raised and written off?

Explanation: When goodwill is raised in the books of the firm at its full value and it is written off, then Goodwill Account is to be credited and all partners' Capital Accounts are to be debited in their old profit sharing ratio.

What is goodwill in a partnership?

Goodwill, at its simplest, is the difference between the fair or market value of the net assets of the partnership and their book value. There are lots of factors that cause that difference, including the market position, expertise, customer base, location, and reputation of the partnership's business.

What shall be the treatment of goodwill in settling the accounts of a firm after dissolution?

In settling the accounts of a firm after dissolution, the goodwill shall, subject to contract between the partners, be included in the assets, and it may be sold either separately or along with other property of the firm.

Is goodwill an expense or income?

Per accounting standards, goodwill is recorded as an intangible asset and evaluated periodically for any possible impairment in value. Private companies in the US may elect to expense a portion of the goodwill periodically on a straight-line basis over a ten-year period or less, reducing the asset's recorded value.

How is goodwill shown on a balance sheet?

Goodwill = Cost of acquisition – Value of net assets Once a business completes the purchase and acquires another business, the purchase is placed on the balance sheet. Goodwill is listed as a noncurrent asset on the balance sheet and is considered an intangible asset since it is not a physical object.

Where do you put goodwill on a balance sheet?

Where Is Goodwill on the Balance Sheet? Goodwill is located in the assets section of a company's balance sheet. Unlike physical assets (like buildings and equipment), goodwill is considered an intangible asset.

What is goodwill in retirement?

Goodwill is the result of overall efforts of all the partners including the retiring one. So at the time of retirement or death of the partner, he/she is entitled to his/her share of goodwill. Let us learn more about the treatment of goodwill.

How to raise goodwill?

Raise the goodwill at its value by crediting all the partners’ capital accounts (including that of the retired/ deceased partners) and then

What is goodwill account?

The goodwill account is debited with the proportionate amount and credited only to the retired/deceased partner’s capital account. Thereafter, in the gaining ratio, the remaining partner’s capital accounts are debited and the goodwill account is credited to write it off.

When goodwill is already appearing in the books of the firm, is it necessary to adjust?

When goodwill is already appearing in the books. Normally no adjustment is required if goodwill is already appearing in the books of the firm. However, goodwill appearing in the books of the firm should be equal to the current value of goodwill.

Is goodwill debited?

In this case, the goodwill account is debited with the excess of its current value over the book value. And all partners’ capital accounts are credited in their old profit sharing ratio.

Who gets goodwill from a deceased partner?

The retiring/ deceased partner gets his share of goodwill from the continuing partners in their gaining ratio. The accounting treatment for goodwill in such a situation depends upon whether or, not goodwill already appears in the books of the firm.

Is goodwill earned by a deceased partner?

The goodwill earned by the firm is the result of the efforts of all the existing partners in the past. Hence, as per agreement among the partners at the time of retirement/death of a partner, goodwill is valued.

What are the elements of goodwill?

The elements or factors that a company is paying extra for or that are represented as goodwill are things such as a company’s good reputation, a solid (loyal) customer or client base, brand identity and recognition, an especially talented workforce, and proprietary technology. These things are, in fact, valuable assets of a company.

What is accounting goodwill?

Accounting goodwill is sometimes defined as an intangible asset that is created when a company purchases another company for a price higher than the fair market value of the target company’s net assets. But referring to the intangible asset as being “created” is misleading – an accounting journal entry is created, ...

What is the amount of economic goodwill created?

If Company B purchases Company A for $250,000, the amount of economic goodwill “created” would be the purchase price minus the fair market value of net assets: $250,000 – $209,000 = $41,000.

What is a takeover premium?

Takeover Premium Takeover premium is the difference between the market value (or estimated value) of the company and the actual price to acquire it.

Is goodwill accounting or economic?

Accounting vs. Economic Goodwill. Goodwill is sometimes separately categorized as economic, or business, goodwill and goodwill in accounting, but to speak as if these were two separate things is an artificial and misleading construct. What is referred to as “accounting goodwill” is really just the recognition in the accounting ...

Is goodwill an asset?

The entry of “goodwill” in a company’s financial statements – it appears in the listing of assets on a company’s balance sheet – is not really the creation of an asset but merely the recognition of its existence.

Does goodwill need to be amortized?

They are designed to maintain credibility and transparency in the financial world. , goodwill is an intangible asset with an indefinite life and thus does not need to be amortized. However, it needs to be evaluated for impairment yearly, and only private companies may elect to amortize goodwill over a 10-year period.

How Do You Record Goodwill In A Partnership?

Taking equity as equal to fair value and stock in return for reducing the withdrawal partner’s assets in cash is recorded as goodwill, as an amount allocated for partner losses, which goes toward all partners.

What Is The Accounting Treatment Of Goodwill?

As a result of the goodwill, the asset or business has a net value far higher than its asset-to-liability value (purchase consideration). Since an intangible asset cannot be seen or touched, it belongs to the financial risk management realm.

How Is Goodwill Treated In Partnership Dissolution?

If a relationship between a party and a company dissolves, goodwill does not need to be treated in a special way. In the same way as any other asset, it should be treated in the same manner. Upon taking the business over, a partner’s capital account is debited and the Realisation Account credits when the settlement sum is reached.

Where Is Goodwill In Partners Capital Account?

By the definition of Hidden Goodwill, the difference between firm capitalizations, and firm assets, are interpreted to reflect net value. Thus, the Inferred Goodwill is hidden Goodwill. This form is not presented in question, it is indicated by his partner’s capital as he seeks to raise capital for his share.

How Is Goodwill Treated In Balance Sheet?

The financial statement shows how Goodwill is used. goodwill of $100 thousand, which exceeds its other assets, can be recognized on its balance sheet. As long as goodwill values remain at the same or an increase occurs, a dollar amount still remains entered. There is also the possibility that goodwill will decline, however.

What Is Goodwill In A Partnership?

How does Goodwill fit into a partnership?? As a result of an acquisition, partnerships lose goodwill. There will be the value of goodwill in the target company to which an acquirer will pay this payment. Using fair value market measures as a guideline, the value per share is determined by the target company’s net assets.

Is Goodwill Shown In Partners Capital Account?

Debits are made with proportionate amounts resulting in capital account credits for both individuals who died and those who retired or left. At this point, the remaining partner’s capital accounts are debited and the goodwill account is credited for the write-off.

What is goodwill? What are some examples?

What is a goodwill? A simple realistic example is when you have something (maybe a toy, shirt, PC games or etc) that you wouldn’t want to give away to your friend, but your friend insisted on having them. In that case, you might be selling them at a higher price, say a limited edition toy that you purchased originally at $100 and your friend are willing to use $120 to purchase the toy (and it is also the price you are willing to give away.) You settled the deal because $120 is attractive! This extra $20 is actually the goodwill.

How to apportion goodwill?

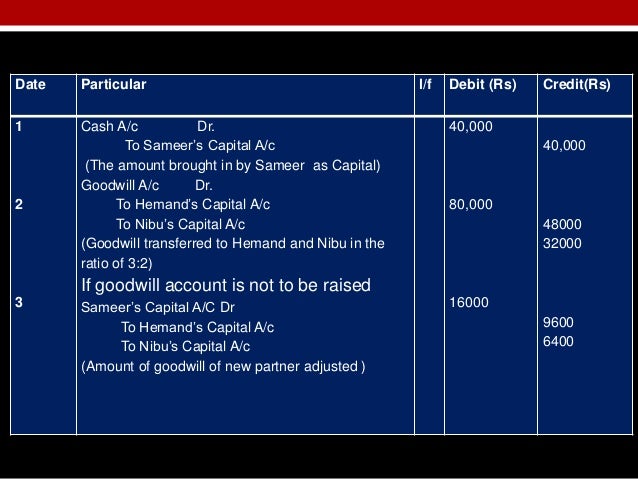

1) For goodwill to be opened, you only apportion using OLD ratio. Whilst for goodwill not to be opened, remember to apportion using both ratio. 2) When preparing for balance sheet, do make sure to include goodwill account in intangible asset (if goodwill account is to be opened). 3) Remember the formats well.

How to open a goodwill account?

The steps to opening a goodwill account can be summarised as shown below: 1) Open a goodwill account and Dr the Goodwill amount based on old profit sharing ratio (Note that goodwill is an intangible asset) 2) Open up a capital account with opening balance and CR goodwill in Capital Account.

How to show goodwill in a company?

1) existing partners wanted to change profit and loss sharing ratios , 2) new partner is introduced, and. 3) one of the partners retires or dies. There are two ways in showing goodwill, one is to show them in the balance sheet (open a goodwill account) and the other one is to not show them in the balance sheet (do not open a goodwill account). ...

Does goodwill need to be maintained?

Since goodwill account is not to be maintained, you skipped the need to open up a goodwill account and then did all the adjustments required in the capital accounts by debiting and crediting capital accounts (increase and decrease by $4,000 resulting in no movement in capital account – see below) but does affect the individual partners.

Is Goodwill account complicated?

For the complicated bit will be where goodwill account is not to be opened. Even though it’s complicated but you don’t actually need to do a lot of work! It’s really just a one step working.

Is goodwill included in the balance sheet?

So, if goodwill account is to be opened, you will actually find goodwill to be included in the balance sheet, increasing the total assets and that the two steps that you have done earlier will also help you to arrive at the new capital balances. For the complicated bit will be where goodwill account is not to be opened.

What is goodwill in a sale?

Goodwill as Part of a Corporate Asset Sale 1 When a corporation is sold in an asset sale, a separate sale of a shareholder's personal goodwill associated with the corporation can result in the gain from the sale of the goodwill being taxed to the shareholder at long-term capital gains rates. 2 Personal goodwill can be present when the owner's reputation, expertise, skill, knowledge, and relationships with customers are critical to the business's success and value. 3 Personal goodwill may be deemed an asset of the corporation where shareholders have transferred the goodwill to the corporation through noncompetition, employment, or other agreements with the corporation. 4 A sale of corporate assets and personal goodwill should be carefully planned and executed to establish that personal goodwill exists and that it is being sold in a separate transaction from the sale of the assets of the corporation.

What is business goodwill?

Business goodwill is an intangible asset owned by and associated with the operation of the business entity.

How do shareholders own goodwill?

To own personal goodwill, a shareholder must be intimately involved in the target corporation. Otherwise, any goodwill acquired by the target corporation would be largely due to the work of others. Thus, almost always, the target corporation will be closely held. In addition, personal goodwill is frequently found in highly technical, specialized, or professional corporations. Furthermore, shareholders of corporations with few customers or suppliers may own personal goodwill from the development of close relationships. Obviously, if a target corporation depends highly on a small number of customers or suppliers, then its shareholders must cultivate these relationships to ensure the corporation's survival. Finally, personal goodwill is more likely to be found if a target corporation's employment agreements with its shareholders are terminable at will or do not contain automatic renewal provisions and there are no restrictive noncompete covenants between the corporation and its shareholders.

How much is goodwill taxable?

A sale of personal goodwill, if respected by the IRS, creates long-term capital gain to the shareholder, taxable at up to 23.8% (maximum capital gain rate of 20%, plus the 3.8% net investment income tax) rather than ordinary income to the target corporation, taxable at up to 35% plus an additional tax of up to 23.8% on the remaining balance of the purchase price distributed by the target corporation to the shareholder, leaving the shareholder with potentially approximately 76 cents rather than 49 cents for every dollar of value for goodwill after federal income tax.

When a corporation is sold in an asset sale, a separate sale of a shareholder's personal goodwill?

When a corporation is sold in an asset sale, a separate sale of a shareholder's personal goodwill associated with the corporation can result in the gain from the sale of the goodwill being taxed to the shareholder at long-term capital gains rates. Personal goodwill can be present when the owner's reputation, ...

Is goodwill sold in a separate transaction?

A sale of corporate assets and personal goodwill should be carefully planned and executed to establish that personal goodwill exists and that it is being sold in a separate transaction from the sale of the assets of the corporation . Selling a business can require some of the most important tax planning an owner may ...

Who owns personal goodwill?

In contrast, personal goodwill is owned by the shareholders of the target corporation and exists when a shareholder's reputation, expertise, skill, and knowledge, as well as the shareholder's contacts and relationships with customers and suppliers, give a business its intrinsic value. Stated somewhat differently, personal ...

What is goodwill in business?

Goodwill is a type of intangible asset that may arise when a company acquires another company entirely. Because acquisitions are designed to increase the value of the combined firm, the purchase price paid often exceeds the book value of the acquired company.

Why does goodwill exist?

Goodwill can exist for many reasons. A business may be willing to pay more than the book value because the business in question may have great profit margins, exceptional future profit growth prospects, or a major competitive advantage.

What is goodwill on the balance sheet?

Goodwill is an intangible asset account on the balance sheet. This series of entries adds the $800,000 in assets to the books, adds the $200,000 in Goodwill, and subtracts $1 million in cash from the books to reflect cash leaving to fund the purchase. Test the goodwill account for impairment each year.

What is goodwill book value?

Book value is the tangible assets of a business minus its liabilities (also known as its debt and its intangible assets). It is called book value because this is the value of the business that is being carried on the balance sheet.

How to calculate goodwill?

To calculate it, simply subtract the total asset market value amount from the purchase price; this amount is nearly always a positive number. For example, consider a firm that acquires another firm for $1,000,000.

What happens if the value of Goodwill drops to $800,000?

If the market value drops to $800,000, would would need to reduce Goodwill by $200,000 to reflect the drop in the value of the assets.

When is goodwill tested?

Test the goodwill account for impairment each year. Each year, Goodwill needs to be tested for something known as impairment. Impairment occurs when something bad happens to a business, which causes the market value of it's assets to decline below the book value. When this happens, Goodwill needs to be reduced by the amount the market value falls below the book value.

How long is goodwill amortized?

Goodwill amortized over 15 years and tax deductible. GAAP accounting. Goodwill tested annually for impairment for public companies. Private companies may choose to amortize goodwill over a period not to exceed 10 years instead.

Is goodwill tax deductible?

Any goodwill created in an acquisition structured as a stock sale is non tax deductible and non amortizable. At the risk of stating the obvious, tax-deductible goodwill is attractive to an acquirer because it will reduce acquirer taxes going forward after the acquisition.

Is goodwill amortized under GAAP?

Under GAAP (“book”) accounting, goodwill is not amortized but rather tested annually for impairment regardless of whether the acquisition is an asset/338 or stock sale. A caveat is that under GAAP, goodwill amortization is permissible for private companies .